A data-driven analysis of 1,000+ HBM patent families reveals who owns the IP landscape for AI memory by 2030.

If you bought a server-class GPU in the last twelve months, you paid for High Bandwidth Memory. If you tried to buy consumer DDR5 in the last six, you paid through the nose, because HBM ate the fab capacity that used to make your DRAM. The 2024-present global memory shortage, what tech press has taken to calling "RAMmageddon," isn't really a shortage. It's a reallocation. And the three companies pulling the wafers are Samsung, SK hynix, and Micron.

So the natural question for anyone watching the AI compute stack: who's going to own the IP under HBM4 and HBM4E by the end of the decade?

We ran the patent corpus to find out. Here's what IP Author's analysis of 1,000+ deduplicated patent families and three US prosecution dockets says about the next five years.

The strategic contextWhy HBM Is Now the Center of Gravity in DRAM

HBM is a 3D-stacked DRAM architecture co-developed by Samsung, AMD, and SK hynix, standardized by JEDEC as JESD235 in October 2013, the same year SK hynix shipped the first commercial chip. The technology stacks up to 32 DRAM dies plus an optional base die, all connected by through-silicon vias and mounted on a silicon interposer beside the host processor.

In 2026, every meaningful AI accelerator on the market (the NVIDIA H100, H200, B100, B200, AMD MI300X, MI325X, Google TPU v5, Intel Gaudi) runs on HBM. HBM3E is shipping in volume today. HBM4 is the active battleground, with Samsung's 1c DRAM line dedicating 60,000 wafers per month to HBM4 production by September 2025. Kearney's PERLab forecasts the underlying memory constraint will persist through 2030.

When we talk about who "wins" HBM4 patents, we're talking about who owns the legal scaffolding for the most strategic component in AI infrastructure.

The dataWhat the Patent Corpus Actually Shows

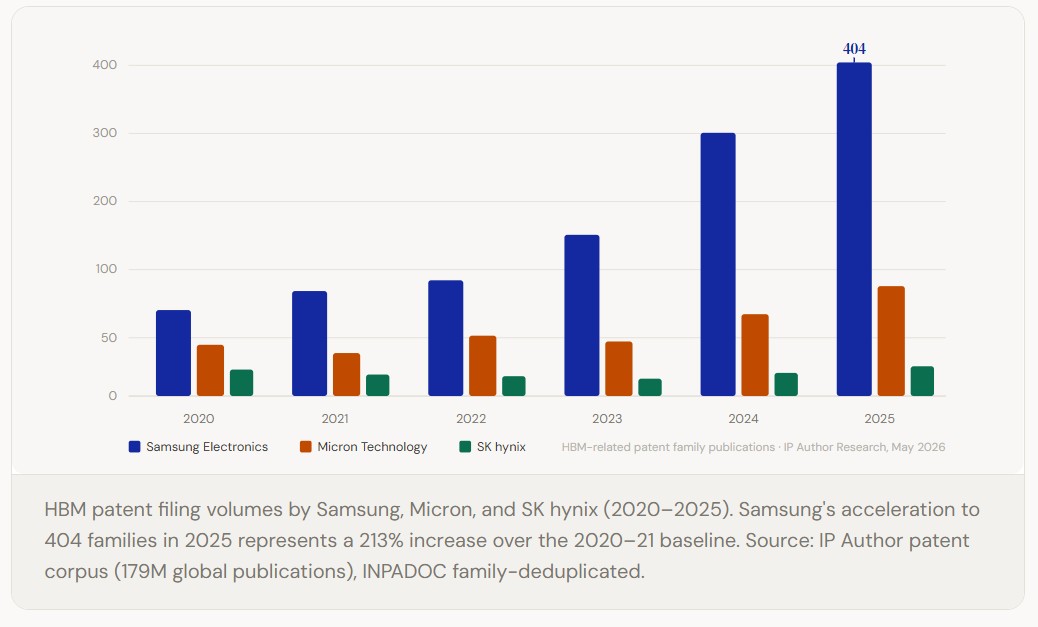

A naive search for "HBM4" returns just 21 patent families globally. That's not because the IP isn't being filed; it's because patent counsel describe the underlying mechanics (stacked DRAM, base die, 2048-bit interface, pseudo-channels, hybrid bonding) rather than naming the JEDEC standard. The economically real corpus, as tracked by IP Author, is the broader HBM/stacked-DRAM cluster from 2020 onward.

| Filer | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 YTD | Total | Acceleration* |

|---|---|---|---|---|---|---|---|---|---|

| Samsung Electronics | 104 | 127 | 140 | 195 | 319 | 404 | 52 | 1,341 | +213% |

| Micron Technology | 62 | 52 | 73 | 66 | 99 | 133 | 46 | 531 | +104% |

| SK hynix | 32 | 26 | 24 | 21 | 28 | 36 | 1 | 168 | +10% |

*Acceleration = 2024-25 filings vs 2020-21 filings. Source: IP Author patent corpus, INPADOC-deduplicated, May 2026.

Three things stand out immediately:

Filing at scale and accelerating

404 HBM-related inventions published in 2025 alone, nearly 4x their 2020 baseline. The only filer with global enforcement breadth across US, KR, CN, EP, JP, and IN.

The steady builder

~500 families across the period, doubling their filing rate, with a US-heavy strategy (80% of their portfolio is US-published). The most efficient prosecution conversion of the three.

Low count, high legacy value

The market leader in HBM (~50% share) yet the lightest filer. Korea-first families collapse in family deduplication; applying a 2-3x correction still leaves them well behind Samsung.

The Geographic Enforcement Story

Patent counts only matter where you can enforce them. Here's where each player has actually filed:

- Samsung: US (958), KR (198), CN (110), EP (26), JP (23), IN (17) - the only one buying global enforcement breadth.

- Micron: US (426), CN (66), EP (16), KR (6) - US-anchored, with a quiet but real China presence.

- SK hynix: US (99), KR (39), CN (29) - the narrowest footprint, asymmetrically strong on home turf.

If you're an AI accelerator vendor assessing FTO exposure, Samsung's portfolio sits in every jurisdiction where you'd ship chips. Their geographic moat is the widest by a significant margin.

What the US Prosecution Funnel Reveals

Filing is one thing. Converting filings to granted patents is another entirely. Here's the current US pipeline across all technology domains, not just HBM, which signals each company's overall prosecution machine. Data sourced from the IP Author US prosecution database:

| Filer | Total US apps | 2024 grants | Pending OAs | Avg pendency |

|---|---|---|---|---|

| Micron Technology | 22,740 | 1,866 | 376 | 1,086 days |

| SK hynix | 14,620 | 760 | 212 | 1,445 days |

| Samsung Electronics | 12,938 | 1,358 | 232 | 2,235 days |

This is where Micron looks unexpectedly powerful. The largest cumulative US filing base, the shortest prosecution pendency (under three years), and the deepest active office-action queue; their attorneys are converting filings to grants faster than either competitor. Samsung's 2,235-day average is nearly twice the field; their issued US position lags their filed position by roughly three years.

SK hynix's open docket is heavy on memory-stack and package architecture: "Stack Packages Including Bonding Wire Interconnections," "Method of Manufacturing Semiconductor Device." That's the HBM technology stack showing up directly in active prosecution.

The 2030 Prediction

Extrapolating the 2020-2025 trajectory linearly through 2030 puts Samsung at roughly 3,500-4,500 cumulative HBM-related families, versus 1,400-1,800 for Micron and 350-500 for SK hynix. Even applying a generous 2-3x upward correction to hynix for Korea-jurisdiction undercount, Samsung still leads by approximately 3:1.

But raw count isn't the only axis that matters.

SK hynix retains an asymmetric position because they own the foundational HBM patents from 2010-2015, specifically the JESD235 era. Those patents carry 20-year terms running through 2030-2035, and they carry weight no later filing can displace. Combined with their dominant NVIDIA supply relationship, hynix punches well above their filing count in the legacy HBM/HBM2/HBM3 claim space.

The new HBM4-era IP (2048-bit interface design, hybrid bonding for stacked DRAM, custom logic base die, pseudo-channel architecture) is being filed by Samsung at roughly 8x hynix's rate. By 2030, Samsung will own the bulk of the HBM4 and HBM4E claim landscape, even as hynix retains the foundational layer below.

Micron is the dark horse. They can't catch Samsung on volume, but their prosecution conversion is the most efficient of the three. In specific sub-areas such as pseudo-channel architecture and DRAM-die encryption, they may end up with the strongest US-issued position per dollar of legal spend.

Who wins

Final Ranking: End of 2030

-

1Samsung ElectronicsWins on count by ~3:1, broadest geographic moat across six jurisdictions, heaviest fab commitment with 60K wafers/month dedicated to HBM4. The patent strategy mirrors the manufacturing strategy.

-

2SK hynixWins on quality-per-patent thanks to foundational HBM IP from the JESD235 era and unmatched customer leverage with NVIDIA. Loses relative share through 2030 but retains the bedrock claim layer.

-

3Micron TechnologyWins on prosecution efficiency. Narrower HBM-specific footprint, but the most likely upside surprise, particularly in pseudo-channel architecture and DRAM-die encryption sub-areas.

Three Things That Could Change This Forecast

A SK hynix-TSMC base-die partnership

TSMC and hynix are co-developing the HBM4 logic base die. A serious joint patent push could 2x hynix's relevant filings between 2026 and 2028, meaningfully closing the count gap.

Samsung HBM4 yield collapse

Credible reports of HBM3E qualification issues with NVIDIA in 2024-25 existed. If Samsung's HBM4 ramp stumbles, engineering bandwidth shifts to firefighting and filing velocity decelerates.

A Chinese entrant disruption

CXMT is filing aggressively in stacked DRAM and could force hynix and Samsung into defensive continuation strategies that distort the headline numbers and divert prosecution resources.

Strategic implications

The Practical Implication for Licensing Strategy

Samsung wins on count. SK hynix wins on quality-per-patent. Micron wins on prosecution efficiency. But by any defensible patent metric, the headline lead in HBM technology IP by 2030 goes to Samsung Electronics, and the gap is widening, not closing.

For anyone licensing into or building products around HBM4, the practical implication is consistent regardless of which metric you weight: you need a license posture that covers Samsung's volume and hynix's foundational position. Micron is a third-party hedge worth pricing into the deal. Explore the full patent landscape at IP Author.

Analysis based on the IP Author patent corpus (179M global publications), US prosecution database, and JEDEC standards records. Patent counts are extended-INPADOC family-deduplicated. Data is point-in-time as of May 2026.

Explore IP Author's Free Prosecution Intelligence Tool

No commitment required. Pull examiner data for your next active application and see what prosecution intelligence actually looks like in practice.